Before I was blind and now I can see. I finally got to read Brad Feld‘s book Venture Deals and now understand the ins and outs of a Term Sheet. I wish I read it earlier. This book is loaded with important content every founder who ever wants to raise money or has raised money should know. Venture Deals helps you understand the VC Game better. Life is a game. You either level up or get lost in its artifacts. Raising money is one of those big games that will affect you for years to come.

The content below is a breakdown of stuff I learnt about Term Sheets from the Venture Deals book with some of my own sprinkle of stories among it. You may also want to read about “The Players” to understand investors and their drivers.

We often hear the word “Term Sheet” being thrown around when raising money. So what is it and what do you need to understand about it?

A Term Sheet is a Blueprint for your future relationship with your investor.

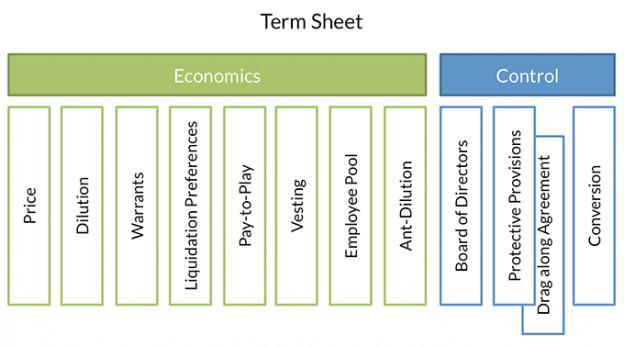

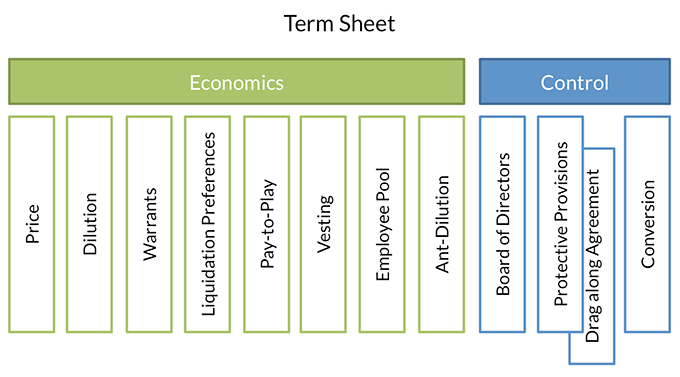

When raising money the VC you are dealing with should only care about:

- Economics: This is the return at a time of liquidity + the terms that directly impact the return

- Control: Mechanisms that allow VC to exercise control over business / veto decisions.

Anything else Brad says, “they are blowing smoke”.

If you see something missing then this is assumed to be less relevant in the grand scheme.

1. The ECONOMICS of a Term Sheet

Price

Price per share is the ultimate measure of what is being paid for the equity bought. This is sometimes called valuation and it comes in 2 forms:

- Pre-money: value before investment and

- Post-money: pre-money + investment.

Example: “I’ll invest $5m at $20m” – post money yields selling 25% of your company while pre-money is 20%.

Brad says, “Always clarify. I assume you mean $20m pre-money?”. The difference here is 5% of your company. That is nothing to sneeze at.

Dilution

Fully diluted / employee pool / option pool

- The size of the pool eats into the company’s valuation. This is Trap #2.

- “I’ll invest $5m at $20m pre-money with 10% option pool” gives you a $18m pre-money valuation.

- Have an option budget listing hires until next round. This minimizes VC risk of future dilutions.

Warrants

This is the right to buy shares at a predefined price for X years. Warrants are commonly used during a bridge load to shame position until future investor comes in. If you want to diversify your investments, you can look into crypto trading at https://immediate.net/de/. Additionally, for comprehensive guidance on crypto trading and investment strategies, consider exploring the Kiana Danial course. Such courses can equip you with valuable knowledge to make informed decisions in the dynamic world of cryptocurrency.

How VC’s value companies

It’s important to understand that valuing companies is hard. There is no exact science. A company is really worth only what someone is willing to pay for it. For example; VC (private investor) agrees to invest X at Y valuation or after an IPO the public investor wants to buy X shares in your company at value Y.

But how does a private investor (a VC) work out the value?

- Early Stage (Seed): Experience of entrepreneurs amount of money being raised and perception of overall opportunities.

- Mature (Series A+): Historical financial performance and future financial solutions required.

- Get several VCs interested in your financing (Demand vs Supply)

- Experienced entrepreneurs == less risk == higher valuation. Also remember this when looking for a cofounder for your new venture. You could also kjope kryptovaluta to diversify your investments.

Liquidation Preferences

This is a term used in venture capital contracts to specify which investors get paid first and how much they get paid in the event of a liquidation event such as the sale of the company. 2 parts to this:

- Actual preferences: money x times returned

- Participation

- Full: Double dips. Means the investor will get their return outside everyone else (common) and then also participates in the options split (less common).

- Capped: Cap when x times $ returned

- No: No double dibs just return based on their company ownership.

IPO removes liquidity event since an IPO is a funding round and prefered stock counts to common stock.

In early stage of financing, its actually in the best interest of both the investor and the entrepreneur to have a simple liquidation preference and no participation.

Pay-to-Play

Investors must participate in future financing (paying) in order to not have their preferred stock converted to common stock (playing) in the company.

Vesting

Is the process by which an employee accrues non-forfeitable rights over employer-provided stock incentives or employer contributions made to the employee’s qualified retirement plan account or pension plan.

- Typically stock and options will vest over 4 years with 1 year cliff (1 off 25% vesting at year 1).

- Cliff encourages the individual to be with the company for at least 1 year to get their stock. After the 1 year stock then vests on a monthly basis.

- Founders vest 1 year upfront at financial and then 36 month after. This 1 year upfront is to incentives them for their hard work pre-funding.

Employee Pool

Also known as option pool is a way of attracting talented employees to a startup company. It is reserved for future insurance to employees. Learn about Hyland business insurance plans for security.

Anti-Dilution

A provision used to protect investors in the event a company issues equity at a lower valuation than in previous financing rounds.

You may hear Weighted average and Ratchet-based anti-dilution They are common in financial and focus on mining their impact and build value in your company. For more on business handling, read here about the best Private equity firm of Australia.

2. The CONTROL of a Term Sheet

Board of Directors

The board is your inner sanctum, your strategic planning department, and your judge, jury and executioner all at once. Andreessen Horowitz (a16z) has a series of podcasts about the Board which I highly recommend.

Protective Provisions

These are veto rights that investors have on certain actions by the company. eg. sell the company, change board size, pay dividend, borrow money etc. These don’t eliminate ability to do them, but simply require consent of the investors.

Sometimes, a Drag-along Agreement may be present which gives the rights to a subset of investors to drag the rest of investors and founders to a specific action eg. sale of a company (fire sale).

Conversion

VCs (preferred shareholders) have the right at any time to convert their stake into common stock. Conversion is done if a sale deal is better for the investor. Once converted, they can’t go back.

TIP: Do not allow investors to negotiate different automatic conversion terms for different series of preferred stock. This can end up in IPO nightmare. Equalize the automatic conversion threshold among all series of stock at each financing.

And that concludes the Blueprint for your future relationship with your investors, the Term Sheet. So, when raising venture capital, make sure you are focused on:

- Economics: This is the return at a time of liquidity + the terms that directly impact the return

- Control: Mechanisms that allow VC to exercise control over business / veto decisions.

Anything else is just blowing smoke.

Feel free to leave comments below.

—

Credit goes to Brad Feld‘s book Venture Deals which helped shed insight into the VC landscape. This should be on every founder’s book shelf and a prerequisite reading material for all entrepreneurs wanting to raise capital.

~ Ernest