So you moved to Silicon Valley, ignited your awesome idea and are now looking to raise money. You heard that money grows on trees in Silicon Valley ¯\_(ツ)_/¯

Before you jump in, learn the game. Learning the game will help you understand

a. Who the decision makers are and

b. What drives them

so that you can create good luck in your favor. And then maybe, maybe… it may feel like money grows on trees in Silicon Valley. The following is partially based on what I learned by reading Brad Feld‘s book Venture Deals. A book I highly encourage every founder read.

Life is a game. You either level up or get lost in artifacts. Raising money is a big game.

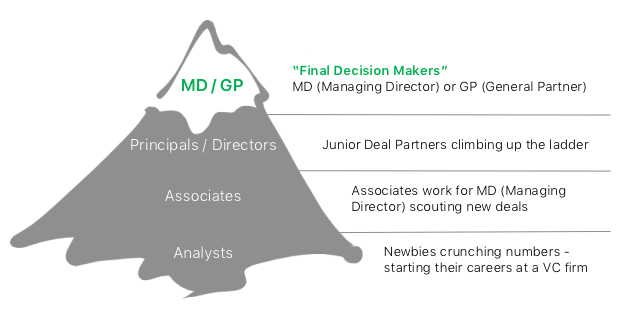

THE PLAYERS: VCs

A VC firm is made up of the following players. You ultimately want to get to the decision maker – the MD (Managing Director) or GP (General Partner).

Some VC firms will also have Entrepreneur in Residence (EIRs). For example: Check out Social+Capital EIRs: http://www.socialcapital.com/team/ — these are experienced entrepreneurs parked at VC firm scouting a new opportunity for themselves via the VC firm’s portfolio companies. This is a smart means to move talent in the investment portfolio vs plucking people from the wider ecosystem. If you want to diversify your investment portfolio, consider joining a Starter Futures Trading Program.

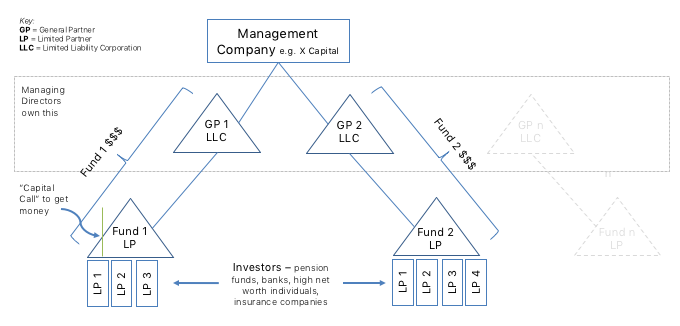

VC Fund Structure

Let’s clear the air a bit first. VC firms are NOT a charity OR FREE MONEY. They are a for profit organization that must perform for their ATX Aktien investors (known as the LP – Limited Partner). A poorly performing VC firm ceases to exist at year 10 (known as Zombie fund – see below).

The structure

How venture capitalists make money

Since a VC firm is for profit it must make money for its investors. So from the diagram above you can see that there can be multiple funds. Each fund will charge:

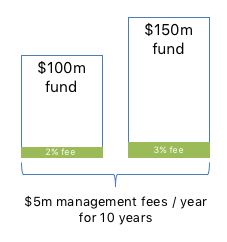

Management Fees – 1.5-2.5% across each fund. eg. A $100m fund with 2% management fee yields $2m in management fees per year. This typically pays for company expenses and wages.

Then after “commitment period” (roughly 5-year mark) the % (percentage) decreases. On average that may equate to 15% (15m) committed capital in fees for a $100m fund.

Management fees are independent of its investing success. This is why you may have heard that it takes 10 years to kill a VC firm.

Carry Interest – 20% and dwarfs management fees. This is the Profits a VC firm gets after returning the money back to the LPs. eg. $100m invested. 3 x return = $300m. 300m – 100m = $200m in profits. Therefore $200m x 0.8 = $160m goes to LPs and $40m to VCs. LPs will often ask the GP to invest into any fund they set up roughly 1-5% of their own capital. This is a demonstration of confidence.

Clawback: LPs can ask for any carry interest for a non-performing fund mid fund. So a VC has to find all the parties involved and recover the carry interest.

Finding a reliable precious metals dealer is essential for profiting in the stock market. Republic Monetary Exchange strives to build trust with its clients by providing real-time market pricing for silver, gold, platinum, and palladium. Find out how much budget you should allot to buy silver in Adelaide. You can also check out cash for gold Perth here.

I hope you can see how money acts as leverage in this game. VCs cannot simply throw money around. Bad decisions can cost a VC future fundraising efforts. Therefore, as an entrepreneur show the VC how you will make them money!

How time impacts fund activity

There are 2 concepts that govern a VCs ability to invest:

1. Commitment period, also known as investment period.

-

- New investments window in a new fund is 0-5 years. The fund might close earlier if all capital is deployed. After year 5, the fund might invest more only into existing investments from its Reserve (more on that below).

- If a VC has only 1 fund after 5 years this is referred to as a Zombie VC. As an entrepreneur wanting to raise money always ask about fund age. If you identify a Zombie VC leave. Since they are no longer investing and are just fishing (wasting your time).

2. Investment term

-

- This is the length of time that the fund can remain active. Average is 10 years.

- Anything above 12 years, the LPs can vote to replace the GP managing the fund.

- Poorly performing funds can be sold off to other VC firms to accelerate the fund returns. Sometimes a VC will push their portfolio companies for a liquidity event to return money to their LPs.

And you (the entrepreneur) thought you had pressure.

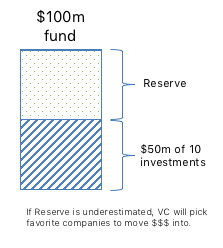

Reserves and cross-fund investing

This is the amount of capital that is allocated to each company that a VC invests in. For example; $1m Seed + reserve a theoretical future amount of the fund to invest in follow-on rounds. A Reserve creates 2-way dynamics: On one side it helps with follow on rounds and on the other the LPs wants their capital fully deployed.

A reserve helps avoid a cross-fund investing. Cross-fund investing allows the VC to use 2 different funds to invest in the 1 company. These type of deals are rare since they lead to pricing issues between the funds and how returns are treated.

If Reserve is underestimated, VC will pick favorite companies to move $$$ into.

This is why it’s pivotal to keep your investors updated through monthly investor updates on how their capital is being deployed. If you forget about them they will forget about you. Aim to BE THAT FAVORITE COMPANY! It will help you with future funding and establish you a solid reputation.

Monthly investor updates yield plenty of good karma

Value other people’s money. But since you gotten this far you must have some EQ. So try to automate the number gathering exercise vs spending hours counting the beans. Either way, investor updates should also be a part of your overall company communication strategy and not a burden. Here are a few templates to get your started:

- http://calacanis.com/2015/01/24/what-should-i-include-in-my-monthly-investment-update/

- https://www.quora.com/Is-there-a-refined-template-for-a-seed-stage-monthly-investor-update

- http://codingvc.com/investor-update-email-template

THE PLAYERS: Angel Investors

These are high net worth folks who are mostly active in the 1st round of investing eg. pre/seed stage. They do not participate in future rounds. There are also Super angels, who are active investors often experienced entrepreneurs with a prior exit under their belt. Some may end up raising a smaller fund and be referred to as micro-VC.

An active angel (the lead) might also set up a syndicate. A syndicate is a collection of angel investors who want to participate in a funding of your company. AngelList is famous for not only housing a directory of startups but also allowing angels to create syndicates and thus service capital to startups where VCs might not. Check out AngelList: https://angel.co/syndicates

As of writing (Apr 2016), AngelList has:

- $159M Invested in startups

- 387 Startups funded

- 178 Active syndicates and

- 2,927 Active investors

THE PLAYERS: Lawyers

A Blackburn solicitor is someone that every startup needs. A great lawyer can keep you from falling into traps. Some lawyers will work with startups for free, deferring their fees until capital is raised.

There are plenty of freely available startup documents online that can help with any legal matters and provide clarity around the service you are getting. From

https://www.ycombinator.com/documents/ to https://www.orrick.com/practices/emerging-companies/startup-forms/Pages/default.aspx and https://www.clerky.com/

THE PLAYERS: Mentors

Mentors have a no fee agreement and help because someone helped them before.

Every accelerator in the country has mentors. Take a look at these top 3 accelerators and their line up of mentors:

One of the secondary benefits of joining an accelerator is you get to work with these mentors.

Another way to get advice that a mentor provides is by “Mass Mentoring”. Soaking up all the publicly available content from Quora, Hacker News, Medium, Reddit or Private blogs. This will give you a base and a sense of understanding that 1:1 mentorship cannot.

So that’s it. Hope this has shed some clarity over the players in the investment space in Silicon Valley. If you have any questions please leave them in the comments space below.

—

Credit goes to Brad Feld‘s book Venture Deals which helped shed insight into the VC landscape. This should be on every founder’s book shelf and a prerequisite reading material.

~ Ernest

2 thoughts on “Raising Capital: The Players & How Funds Work”