En la actualidad, la industria de los juegos en línea atrae a un número creciente de entusiastas. Elegir el proveedor adecuado puede marcar la diferencia entre una experiencia satisfactoria y una decepcionante. Entre los nombres que destacan en este ámbito, Play’n Go se ha consolidado como una opción preferida por muchos jugadores. Para conocer más sobre sus ofertas, visita su sitio web.

La diversidad de juegos que ofrecen diferentes proveedores permite a los jugadores explorar una amplia gama de temas y estilos. Desde tragamonedas emocionantes hasta juegos de mesa clásicos, cada proveedor tiene su propia propuesta única. Analizar las características y la calidad de los juegos de cada proveedor es esencial para disfrutar de una experiencia óptima en 1Win.

Cómo elegir un proveedor de juegos confiable en 1Win

Elegir un proveedor de juegos en 1Win puede ser un desafío, sobre todo por la gran cantidad de opciones disponibles. Un aspecto clave es la calidad de juegos que ofrecen. Marcas reconocidas como Play’n Go y NetEnt son ejemplos de compañías que destacan por su compromiso con la excelencia y la innovación en el desarrollo de juegos.

Además de la calidad de los juegos, es importante verificar la reputación del proveedor. Investigar las opiniones de otros jugadores y leer reseñas puede proporcionar información valiosa sobre la fiabilidad y la experiencia general que se puede esperar. También es recomendable visitar [sus páginas oficiales](https://www.1win.com) para obtener detalles adicionales sobre los juegos, promociones y características únicas que cada proveedor ofrece.

Características clave de los mejores juegos en 1Win

La elección de juegos en 1Win se ve enriquecida por la presencia de proveedores como Play’n Go y NetEnt, conocidos por su compromiso con la calidad de juegos. Estos desarrolladores se destacan por ofrecer títulos innovadores y entretenidos, asegurando experiencias únicas para los jugadores. La diversidad de temáticas y mecánicas de juego es una de las características más valoradas por los usuarios.

Además de la variedad, la jugabilidad es un aspecto fundamental. Los mejores juegos suelen contar con gráficos impresionantes, animaciones fluidas y una interfaz intuitiva que facilita la navegación. El rendimiento de estos títulos es excepcional, con tiempos de carga rápidos y un funcionamiento sin problemas, lo que contribuye a una experiencia de usuario agradable y satisfactoria.

Comparativa de proveedores de juegos populares en 1Win

Al elegir un proveedor de juegos en 1Win, es fundamental evaluar las opciones más destacadas. Este análisis se centra en tres de los proveedores más populares: NetEnt, Play’n Go y Microgaming. Para una revisión completa y más información, visita https://1-win-ar.net/.

NetEnt se ha consolidado como líder en la industria gracias a su amplia gama de tragamonedas y mesas de juegos en vivo. Su enfoque en el diseño gráfico y la innovación de mecánicas les permite ofrecer experiencias únicas que atraen a jugadores de todo el mundo.

Play’n Go, por otro lado, sobresale por la calidad y la diversificación de su catálogo. Sus juegos, que incluyen tanto tragamonedas como opciones de mesa, están diseñados para adaptarse a diferentes gustos, lo que los hace ideales para todo tipo de jugadores. Además, su capacidad para incorporar elementos temáticos originales los distingue en el mercado.

Microgaming es reconocido por su vasta experiencia y legado en la creación de software para casinos en línea. Ofrece una impresionante biblioteca de juegos, combinando clásicos con las últimas novedades. Su plataforma también es conocida por su amplia variedad de jackpots progresivos, que atraen a quienes buscan grandes premios.

Cada uno de estos proveedores tiene características únicas que los hacen preferibles según las preferencias del jugador. Al considerar aspectos como la jugabilidad, la calidad gráfica y la diversidad de temáticas, es posible encontrar el proveedor que mejor se adapte a tus necesidades en 1Win.

Before I was blind and now I can see. I finally got to read Brad Feld‘s book Venture Deals and now understand the ins and outs of a Term Sheet. I wish I read it earlier. This book is loaded with important content every founder who ever wants to raise money or has raised money should know. Venture Deals helps you understand the VC Game better. Life is a game. You either level up or get lost in its artifacts. Raising money is one of those big games that will affect you for years to come.

The content below is a breakdown of stuff I learnt about Term Sheets from the Venture Deals book with some of my own sprinkle of stories among it. You may also want to read about “The Players” to understand investors and their drivers.

We often hear the word “Term Sheet” being thrown around when raising money. So what is it and what do you need to understand about it?

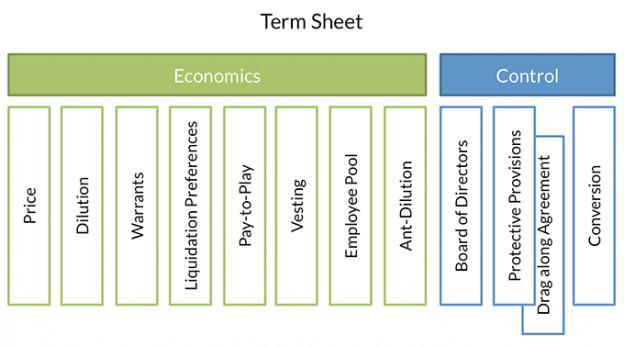

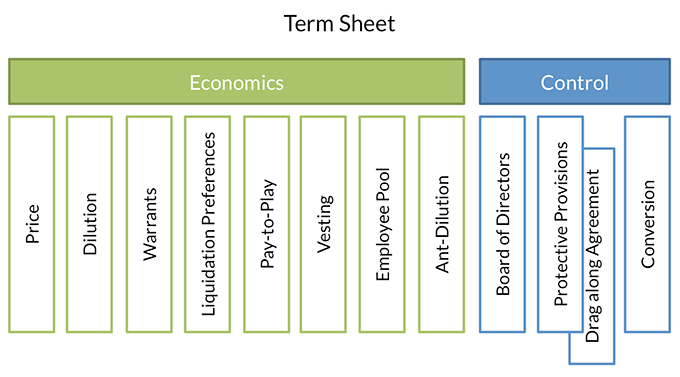

A Term Sheet is a Blueprint for your future relationship with your investor.

When raising money the VC you are dealing with should only care about:

Economics: This is the return at a time of liquidity + the terms that directly impact the return

Control: Mechanisms that allow VC to exercise control over business / veto decisions.

Anything else Brad says, “they are blowing smoke”.

If you see something missing then this is assumed to be less relevant in the grand scheme.

1. The ECONOMICS of a Term Sheet

Price

Price per share is the ultimate measure of what is being paid for the equity bought. This is sometimes called valuation and it comes in 2 forms:

Pre-money: value before investment and

Post-money: pre-money + investment.

Example: “I’ll invest $5m at $20m” – post money yields selling 25% of your company while pre-money is 20%.

Brad says, “Always clarify. I assume you mean $20m pre-money?”. The difference here is 5% of your company. That is nothing to sneeze at.

Dilution

Fully diluted / employee pool / option pool

The size of the pool eats into the company’s valuation. This is Trap #2.

“I’ll invest $5m at $20m pre-money with 10% option pool” gives you a $18m pre-money valuation.

Have an option budget listing hires until next round. This minimizes VC risk of future dilutions.

Warrants

This is the right to buy shares at a predefined price for X years. Warrants are commonly used during a bridge load to shame position until future investor comes in. If you want to diversify your investments, you can look into crypto trading at https://immediate.net/de/. Additionally, for comprehensive guidance on crypto trading and investment strategies, consider exploring the Kiana Danial course. Such courses can equip you with valuable knowledge to make informed decisions in the dynamic world of cryptocurrency.

How VC’s value companies

It’s important to understand that valuing companies is hard. There is no exact science. A company is really worth only what someone is willing to pay for it. For example; VC (private investor) agrees to invest X at Y valuation or after an IPO the public investor wants to buy X shares in your company at value Y.

But how does a private investor (a VC) work out the value?

Early Stage (Seed): Experience of entrepreneurs amount of money being raised and perception of overall opportunities.

If you want a great valuation think back to school when you learnt fundamental concepts of economics and tip the supply relationship in your favor.

Get several VCs interested in your financing (Demand vs Supply)

Experienced entrepreneurs == less risk == higher valuation. Also remember this when looking for a cofounder for your new venture. You could also kjope kryptovaluta to diversify your investments.

Liquidation Preferences

This is a term used in venture capital contracts to specify which investors get paid first and how much they get paid in the event of a liquidation event such as the sale of the company. 2 parts to this:

Actual preferences: money x times returned

Participation

Full: Double dips. Means the investor will get their return outside everyone else (common) and then also participates in the options split (less common).

Capped: Cap when x times $ returned

No: No double dibs just return based on their company ownership.

IPO removes liquidity event since an IPO is a funding round and prefered stock counts to common stock.

In early stage of financing, its actually in the best interest of both the investor and the entrepreneur to have a simple liquidation preference and no participation.

Pay-to-Play

Investors must participate in future financing (paying) in order to not have their preferred stock converted to common stock (playing) in the company.

Vesting

Is the process by which an employee accrues non-forfeitable rights over employer-provided stock incentives or employer contributions made to the employee’s qualified retirement plan account or pension plan.

Typically stock and options will vest over 4 years with 1 year cliff (1 off 25% vesting at year 1).

Cliff encourages the individual to be with the company for at least 1 year to get their stock. After the 1 year stock then vests on a monthly basis.

Founders vest 1 year upfront at financial and then 36 month after. This 1 year upfront is to incentives them for their hard work pre-funding.

Employee Pool

Also known as option pool is a way of attracting talented employees to a startup company. It is reserved for future insurance to employees. Learn about Hyland business insurance plans for security.

Anti-Dilution

A provision used to protect investors in the event a company issues equity at a lower valuation than in previous financing rounds.

You may hear Weighted average and Ratchet-based anti-dilution They are common in financial and focus on mining their impact and build value in your company. For more on business handling, read here about the best Private equity firm of Australia.

2. The CONTROL of a Term Sheet

Board of Directors

The board is your inner sanctum, your strategic planning department, and your judge, jury and executioner all at once. Andreessen Horowitz (a16z) has a series of podcasts about the Board which I highly recommend.

Protective Provisions

These are veto rights that investors have on certain actions by the company. eg. sell the company, change board size, pay dividend, borrow money etc. These don’t eliminate ability to do them, but simply require consent of the investors.

Sometimes, a Drag-along Agreement may be present which gives the rights to a subset of investors to drag the rest of investors and founders to a specific action eg. sale of a company (fire sale).

Conversion

VCs (preferred shareholders) have the right at any time to convert their stake into common stock. Conversion is done if a sale deal is better for the investor. Once converted, they can’t go back.

TIP: Do not allow investors to negotiate different automatic conversion terms for different series of preferred stock. This can end up in IPO nightmare. Equalize the automatic conversion threshold among all series of stock at each financing.

And that concludes the Blueprint for your future relationship with your investors, the Term Sheet. So, when raising venture capital, make sure you are focused on:

Economics: This is the return at a time of liquidity + the terms that directly impact the return

Control: Mechanisms that allow VC to exercise control over business / veto decisions.

Anything else is just blowing smoke.

Feel free to leave comments below.

—

Credit goes to Brad Feld‘s book Venture Deals which helped shed insight into the VC landscape. This should be on every founder’s book shelf and a prerequisite reading material for all entrepreneurs wanting to raise capital.

So you moved to Silicon Valley, ignited your awesome idea and are now looking to raise money. You heard that money grows on trees in Silicon Valley ¯\_(ツ)_/¯

Before you jump in, learn the game. Learning the game will help you understand

a. Who the decision makers are and b. What drives them

so that you can create good luck in your favor. And then maybe, maybe… it may feel like money grows on trees in Silicon Valley. The following is partially based on what I learned by reading Brad Feld‘s book Venture Deals. A book I highly encourage every founder read.

Life is a game. You either level up or get lost in artifacts. Raising money is a big game.

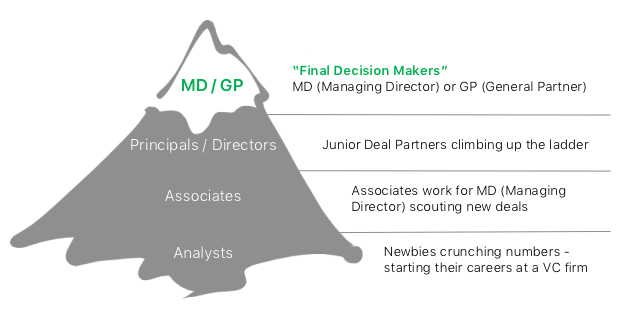

THE PLAYERS: VCs

A VC firm is made up of the following players. You ultimately want to get to the decision maker – the MD (Managing Director) or GP (General Partner).

Some VC firms will also have Entrepreneur in Residence (EIRs). For example: Check out Social+Capital EIRs: http://www.socialcapital.com/team/ — these are experienced entrepreneurs parked at VC firm scouting a new opportunity for themselves via the VC firm’s portfolio companies. This is a smart means to move talent in the investment portfolio vs plucking people from the wider ecosystem. If you want to diversify your investment portfolio, consider joining a Starter Futures Trading Program.

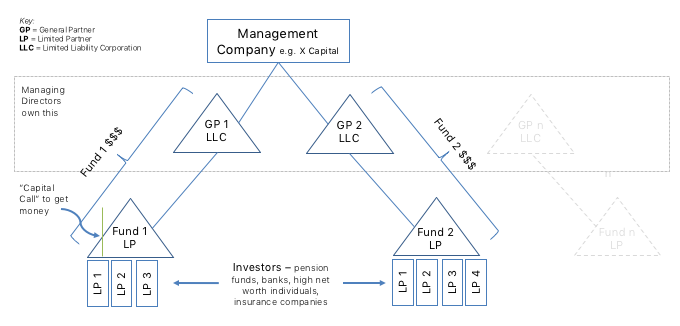

VC Fund Structure

Let’s clear the air a bit first. VC firms are NOT a charity OR FREE MONEY. They are a for profit organization that must perform for their ATX Aktien investors (known as the LP – Limited Partner). A poorly performing VC firm ceases to exist at year 10 (known as Zombie fund – see below).

The structure

How venture capitalists make money

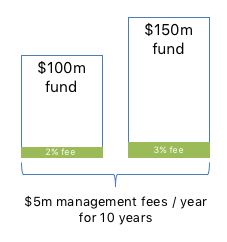

Since a VC firm is for profit it must make money for its investors. So from the diagram above you can see that there can be multiple funds. Each fund will charge:

Management Fees – 1.5-2.5% across each fund. eg. A $100m fund with 2% management fee yields $2m in management fees per year. This typically pays for company expenses and wages.

Then after “commitment period” (roughly 5-year mark) the % (percentage) decreases. On average that may equate to 15% (15m) committed capital in fees for a $100m fund.

Management fees are independent of its investing success. This is why you may have heard that it takes 10 years to kill a VC firm.

Carry Interest – 20% and dwarfs management fees. This is the Profits a VC firm gets after returning the money back to the LPs. eg. $100m invested. 3 x return = $300m. 300m – 100m = $200m in profits. Therefore $200m x 0.8 = $160m goes to LPs and $40m to VCs. LPs will often ask the GP to invest into any fund they set up roughly 1-5% of their own capital. This is a demonstration of confidence.

Clawback: LPs can ask for any carry interest for a non-performing fund mid fund. So a VC has to find all the parties involved and recover the carry interest.

Finding a reliable precious metals dealer is essential for profiting in the stock market. Republic Monetary Exchange strives to build trust with its clients by providing real-time market pricing for silver, gold, platinum, and palladium. Find out how much budget you should allot to buy silver in Adelaide. You can also check out cash for gold Perth here.

I hope you can see how money acts as leverage in this game. VCs cannot simply throw money around. Bad decisions can cost a VC future fundraising efforts. Therefore, as an entrepreneur show the VC how you will make them money!

How time impacts fund activity

There are 2 concepts that govern a VCs ability to invest:

1. Commitment period, also known as investment period.

New investments window in a new fund is 0-5 years. The fund might close earlier if all capital is deployed. After year 5, the fund might invest more only into existing investments from its Reserve (more on that below).

If a VC has only 1 fund after 5 years this is referred to as a Zombie VC. As an entrepreneur wanting to raise money always ask about fund age. If you identify a Zombie VC leave. Since they are no longer investing and are just fishing (wasting your time).

2. Investment term

This is the length of time that the fund can remain active. Average is 10 years.

Anything above 12 years, the LPs can vote to replace the GP managing the fund.

Poorly performing funds can be sold off to other VC firms to accelerate the fund returns. Sometimes a VC will push their portfolio companies for a liquidity event to return money to their LPs.

And you (the entrepreneur) thought you had pressure.

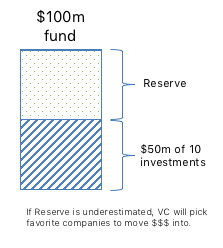

Reserves and cross-fund investing

This is the amount of capital that is allocated to each company that a VC invests in. For example; $1m Seed + reserve a theoretical future amount of the fund to invest in follow-on rounds. A Reserve creates 2-way dynamics: On one side it helps with follow on rounds and on the other the LPs wants their capital fully deployed.

A reserve helps avoid a cross-fund investing. Cross-fund investing allows the VC to use 2 different funds to invest in the 1 company. These type of deals are rare since they lead to pricing issues between the funds and how returns are treated.

If Reserve is underestimated, VC will pick favorite companies to move $$$ into.

This is why it’s pivotal to keep your investors updated through monthly investor updates on how their capital is being deployed. If you forget about them they will forget about you. Aim to BE THAT FAVORITE COMPANY! It will help you with future funding and establish you a solid reputation.

Monthly investor updates yield plenty of good karma

Value other people’s money. But since you gotten this far you must have some EQ. So try to automate the number gathering exercise vs spending hours counting the beans. Either way, investor updates should also be a part of your overall company communication strategy and not a burden. Here are a few templates to get your started:

These are high net worth folks who are mostly active in the 1st round of investing eg. pre/seed stage. They do not participate in future rounds. There are also Super angels, who are active investors often experienced entrepreneurs with a prior exit under their belt. Some may end up raising a smaller fund and be referred to as micro-VC.

An active angel (the lead) might also set up a syndicate. A syndicate is a collection of angel investors who want to participate in a funding of your company. AngelList is famous for not only housing a directory of startups but also allowing angels to create syndicates and thus service capital to startups where VCs might not. Check out AngelList: https://angel.co/syndicates

As of writing (Apr 2016), AngelList has:

$159M Invested in startups

387 Startups funded

178 Active syndicates and

2,927 Active investors

THE PLAYERS: Lawyers

A Blackburn solicitor is someone that every startup needs. A great lawyer can keep you from falling into traps. Some lawyers will work with startups for free, deferring their fees until capital is raised.

One of the secondary benefits of joining an accelerator is you get to work with these mentors.

Another way to get advice that a mentor provides is by “Mass Mentoring”. Soaking up all the publicly available content from Quora, Hacker News, Medium, Reddit or Private blogs. This will give you a base and a sense of understanding that 1:1 mentorship cannot.

So that’s it. Hope this has shed some clarity over the players in the investment space in Silicon Valley. If you have any questions please leave them in the comments space below.

—

Credit goes to Brad Feld‘s book Venture Deals which helped shed insight into the VC landscape. This should be on every founder’s book shelf and a prerequisite reading material.