Healthcare in the US is complicated. The start of each annual calendar is that time of the year. When you get a chance to step outside into the mist and change or join a US health insurance plan. Or maybe you won’t.. in fear of the unknown. You heard all the tales of terror. But maybe this time it might be different. You plough through…

Back in 2009 we were acquired by a US based company. So off I went to Silicon Valley leaving Australia and it’s public healthcare behind. I still remember being presented with a bunch of paperwork outlining health plan options and I was like.. wtf is HMO? Or PPO or Kaiser? Network? There’s a network? Worse, what do all these pages of tabular data mean and how the **** do I compare it all? I was lost in the vastness of options and meaningless pool of words. Later when I became a cofounder of a health tech startup, as an employer, I needed to setup company healthcare for our company and its employees. Being partially prepared and had UK manufacturing health and safety advice helped but I also experienced the other side of the coin.

Today, I feel like having seen both sides of the fence (employee and employer) I can share my experience and hopefully demystify a tad of the US healthcare for newbies. If you’re in need of healthcare services, you may visit a clinic or facility that has professional ABA Billing Services to ensure that your bills and insurance claims are processed efficiently.

Healthcare acronyms – what it all means

- Network: hospitals are owned by a healthcare provider — e.g. PAMF, ECLG, UCSF (all based in SF/Silicon Valley) all are owned by Sutter Health Network. You can find this info on the Network’s website. This is Sutter: http://www.sutterhealth.org/about/affiliates/hospitals.html — pretty big reach. Another Network you may hear about is called Kaiser.

- Health Maintenance Organization (HMO): Coverage limited to your selected Network.

- Preferred Provider Organization (PPO): Like HMP but you have a choice to go outside of your network for an extra fee.

- Insurer: Provider of healthcare plans for HMO, PPO et al, E.g. Blue Shield of California provides plans for Sutter Health Network. Website: https://www.blueshieldca.com/

- Group plan: something your employer sets up with a selected Insurer (eg. Blue Shield of California or a Broken) to provide their employees discounted healthcare coverage options. More on that below.

- Metal Categories: There are 4 categories of health insurance plans (insurance pays/you pay): Bronze (60/40), Silver (70/30), Gold (80/20), and Platinum (90/10).

- Deductible: How much you pay before before your insurance company pays anything. ie. You must pay all the costs up to the deductible amount before this plan begins to pay for covered services you use.

- Copayments and coinsurance: Payments you make each time you get a medical service after reaching your deductible. If you click to read, you’d know that there are many mode of accepted payments, if that’s any consolation.

- Out-of-pocket maximum: Max out of pocket per year. After you reach it, the insurance company pays 100% for covered services.

The EMPLOYEE Hat

Good health and no plan for kids

If you have good health and no plan for kids all you need to care about is:

- What network you want to be part of — typically one in your county (close by) eg. Sutter Health

- How much “Choice” you want eg. HMO in a large network like Sutter is good enough unless your picky about your specialists. But then again your health is good and you have no plans for kids so why bother with PPO.

- Office visits (copayments) — this is how much you will pay for doctor or specialist visits and

- Deductible — the left over bit insurance didn’t cover — how much you want to pay for medication — $5-$25 is acceptable

Pending the size of your employer and if your in tech (Silicon Valley), they will have a bunch of Plans to choose from with different (low) monthly out of pocket. Some smaller companies might not be providing so much luxury and you will have to decide whether to pay extra for the next plan up.

Planning to have kids or have bad health

If your planning to have kids or have health issues then;

- Consider PPO. So you have “Choice” of care.

- A PPO plan has lower out of pocket expenses but costs more.

- Everything mentioned above as HMO also applies here.

Having kids in Silicon Valley is EXPENSIVE

From midwives to duelers to hospitals to all the OB & genetic screening visits, it’s a lot. You want the freedom of choice without too much sacrifice. Hence the advice to go PPO. Expect your insurance company to pay ~$50K for 1 kid delivered at EL Camino Los Gatos Hospital to Stanford Hospital (Sutter network and popular Silicon Valley hospitals). Out of pocket ~$2K. Once you hit the out of pocket (OOP) maximum the Insurer will cover the rest. We hit it on each birth. After you hit the OOP everything is free.

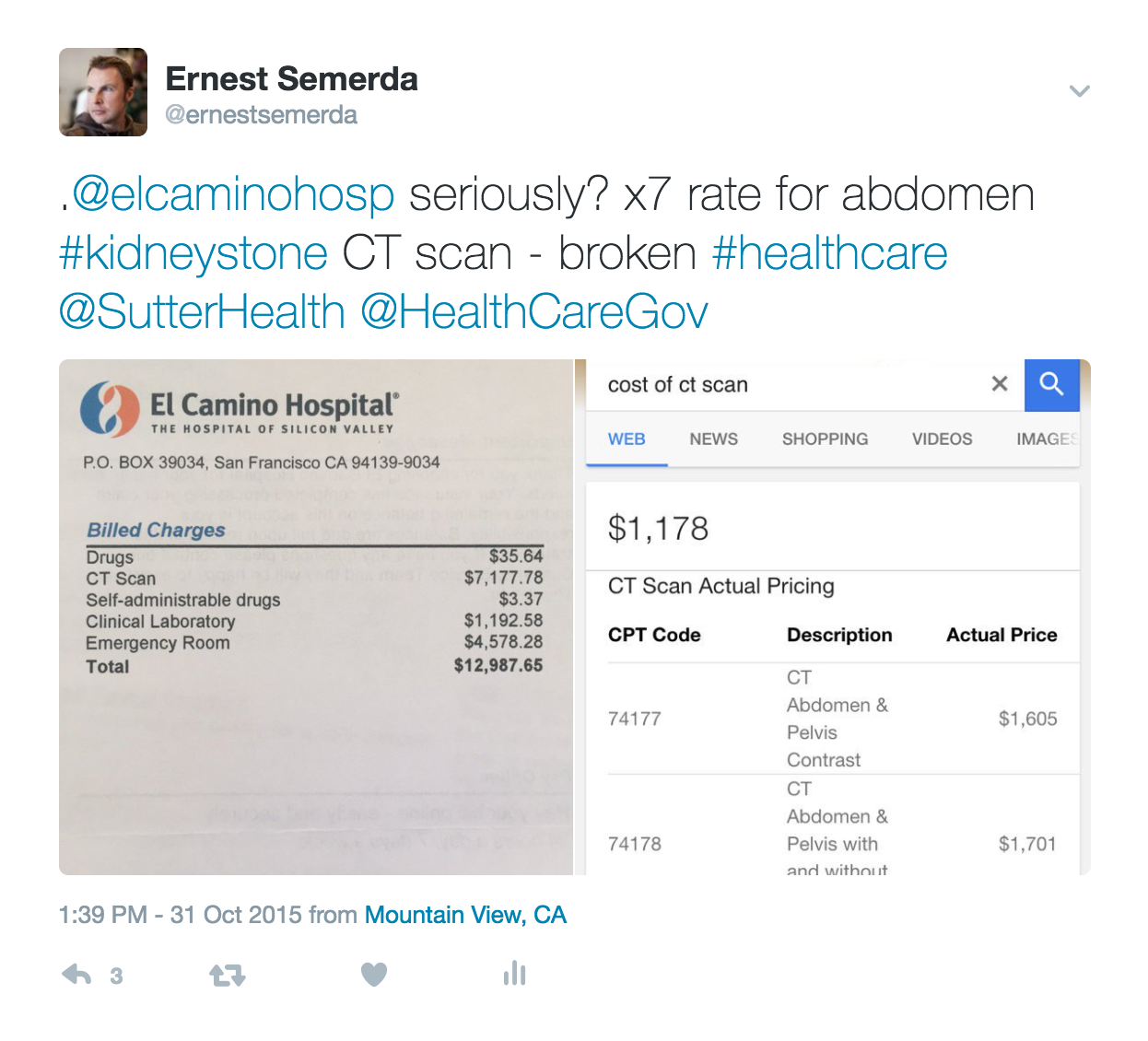

Medical Bills are RIDICULOUSLY INCONSISTENT

Especially emergency visits. Be prepared. How ridiculous & inconsistent? I have no history of kidney stones but thanks to the popular replacement diet popular in Silicon Valley (no name mentioned) landed me in Emergency. Standard resolution CT scan got billed at emergency at 5am for $7K. Total Emergency bill was pushing $10K for 1hr stay. Google “CT Scan” and you’ll see that standard price is $2K for getting smacked with radiation. That inconsistent! Thanks to my amazing Insurer Blue Shield for covering the out of pocket.

The EMPLOYER Hat

Tech companies in Silicon Valley compete for talent using many forms of incentives which also includes healthcare benefits. However startups are at a disadvantage because a 2–5 wo/man shop cannot use Gusto, Zenefits et al Insurers, instead they need a broker to get a Group plan for 2+ employees with “decent benefits”. Look, the [faster] you grow your business the faster you can move to a plan that’s reasonably priced. Don’t fart around moving slow.

Comparing health insurance options for your company is a pain in the bum. It takes time. And provide shitty coverage for your future employees and don’t expect quality candidates. Information is freely available and employees do share with each other their benefits. If you’re also considering a life insurance plan, you can visit this website to compare quotes from multiple insurance providers.

Next be aware of the Insurers coverage not just in your area but also further state wide to cover employees when they travel and need care outside state.

Group plan and group # is what you get from your broker once they have setup healthcare plans for your employees. Once that’s done, hook it into Gusto to make it easy for your employees to handle their health affairs. PAY ATTENTION! This is important. I’ve seen this before where sloppy setups create confusion and friction in the workforce. Automate your HR. Startups with 5+ employees can by pass the independent broker and use Gusto’s network of healthcare Providers.

Other tidbits

Avoid Kaiser Network

In my time in Silicon Valley I never came across anyone in the tech community who chose Kaiser when they had other options. I’ve heard stories of being treated like a number. That speaks louder then my advise here.

Catch an Uber, not an Ambulance

Ambulances are expensive. A fully equipped ambulance is called ALS (Advanced Life System) and costs ~$3K or the basic model BLS (Basic Life System) ~1.5K. If you can walk catch an Uber or a police car take you for free to emergency. The ambulance can stitch you up at the point of accident, thank them and Uber in.

Hospitals will always give you care

Even when you don’t have insurance. So don’t believe the horror refusal of care stories online. There’s always a different side to every story. However the hospital may chase you for large bills after. So get your insurance sorted if your new to Silicon Valley / US.

Hope this shed some light and as an employee or startup founder you are hopefully empowered or more educated to make the right decisions around healthcare. You may also want to know the use of a healthcare software from companies like Foresee Medical, which is mainly used to to estimate future health care costs for patients.

Feel free to contact me with further questions or leave your comments below.

~ Ernest